Your Guide to Commercial UAV Insurance

Flying a drone for your business without the right insurance policy is a bit like driving a delivery truck with your personal car insurance—you might feel covered, but in reality, you're exposed to massive, business-ending risks.

Put simply, commercial UAV insurance is a specific type of policy built to handle the unique aviation risks that your standard business insurance won't touch. It's the one non-negotiable asset you need to protect your company from financial disaster if an accident happens.

Why Commercial UAV Insurance Is a Must-Have

A lot of drone operators fall into the trap of thinking their general business liability policy has their back. This is a dangerous, and expensive, misunderstanding. Nearly all standard policies have an "aviation exclusion" clause, which means any claim related to an aircraft—and yes, that includes your drone—is instantly denied.

This leaves your business completely on the hook for potentially devastating costs from property damage or bodily injury claims. Think of it this way: your business is the house, and commercial UAV insurance is the foundation. Without it, the whole thing could come crumbling down.

This coverage isn't just a nice-to-have safety net; it's a hard requirement for any serious professional operation. High-value clients in sectors like construction, energy, and film production simply won't hire an uninsured pilot. A solid policy is a signal to the market that you're credible, professional, and ready for primetime.

A Rapidly Growing Professional Standard

Just look at the numbers—they tell the whole story. The global commercial UAV insurance market was valued at around USD 1.75 billion in 2024 and is expected to skyrocket to USD 3.82 billion by 2033. This isn't just random growth; it’s a clear sign that proper insurance has become a cornerstone of the industry.

To give a sense of the scale of risk we're talking about, here’s a quick overview of what a good policy is designed to handle.

Key Risks Covered by Commercial UAV Insurance

| Risk Category | Description of Coverage | Real-World Example |

|---|---|---|

| Bodily Injury | Covers medical expenses, legal fees, and settlement costs if your drone injures a person. | Your drone loses power and strikes a bystander at an outdoor event, causing injury. |

| Property Damage | Pays for the repair or replacement of property damaged by your drone during operations. | While inspecting a roof, your drone drifts into a window, shattering it and damaging interior items. |

| Invasion of Privacy | Protects against claims alleging your drone's camera captured private images or data without consent. | A homeowner sues after your real estate photography drone inadvertently films inside their house. |

| Hull & Payload Damage | Covers the cost to repair or replace your own drone (hull) and any attached equipment (payload). | You lose signal, and your drone crashes, destroying both the aircraft and a high-end thermal camera. |

As you can see, the potential for things to go wrong is very real, and the financial consequences can be severe.

In a market this competitive, being properly insured is one of your biggest advantages. It shows you’re committed to safety and professionalism, opening doors to the kind of large-scale enterprise projects that are completely off-limits to uninsured operators.

Beyond Accidents: Building a Credible Business

At the end of the day, having the right policy is about more than just managing accidents—it's about building a business that clients can trust. It proves you take risk seriously and have the financial backing to make things right if the unexpected happens.

This kind of preparation is fundamental to effective drone risk management and is what separates the hobbyists from the true professionals. In the sections that follow, we'll break down exactly what types of coverage you need to make sure your operations are built on a solid, insurable foundation.

Decoding Your Policy: What Coverage Do You Actually Need?

Stepping into the world of commercial UAV insurance can feel like trying to read a foreign language. With terms like "hull," "payload," and "liability" flying around, it’s easy to get lost. But getting a grip on these core components is the key to building a policy that truly protects your business—without you paying for coverage you don't need.

Think of it like putting together a toolkit. You don’t need every tool ever made, just the right ones for the jobs you do. Let's break down the essential types of coverage, piece by piece, so you can assemble the perfect toolkit for your operations.

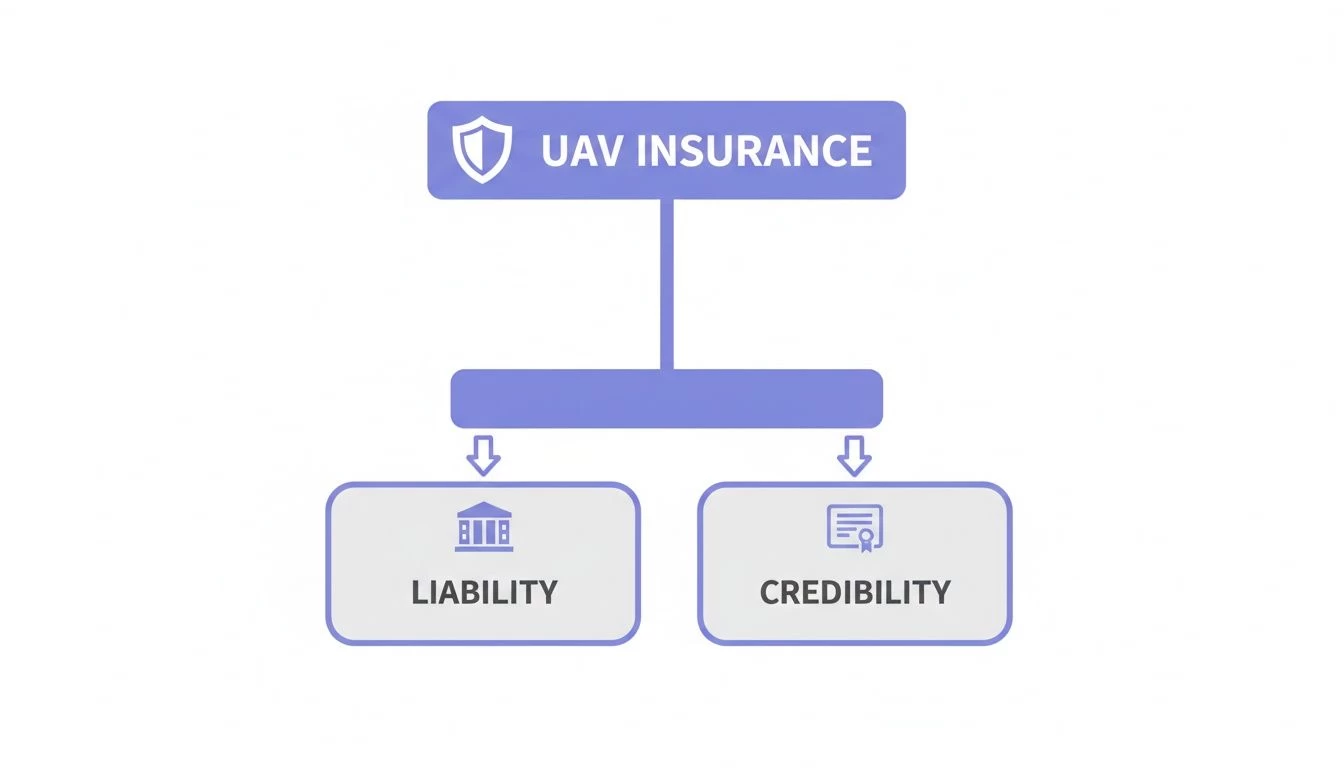

The Cornerstone of Protection: Liability Coverage

First up, and most importantly, is liability coverage. This is the non-negotiable foundation of any commercial drone insurance policy. It protects you from the financial fallout if your drone causes bodily injury to a person or damages someone else's property.

Imagine you're doing a roof inspection. A sudden gust of wind sends your drone into a large window on the neighbouring property, shattering it. Without liability insurance, you're on the hook for the repairs, which could easily run into thousands. With it, your policy steps in to cover those costs.

Because it’s so critical for protecting against third-party claims, liability coverage is the biggest piece of the commercial UAV insurance market. This is especially true in North America and Europe, where drone use is widespread and regulations often require this protection for any professional flight. You can read more on the drone insurance market to see how these trends are shaping the industry.

The image below shows just how central liability coverage is to building a credible, professional operation.

As you can see, a solid insurance plan is built on a foundation of liability protection. Get that right, and you're well on your way to establishing your business's credibility.

Protecting Your Own Gear: Hull and Payload Coverage

While liability covers damage to others, what about your own expensive equipment? That's where hull and payload coverage come in. These two are often bundled together but cover different parts of your setup.

- Hull Coverage: This is for the drone itself—the physical airframe, motors, and all the integrated systems. If you lose signal and your drone takes a nosedive into a tree, hull coverage pays to repair or replace the aircraft.

- Payload Coverage: This protects the valuable gear you attach to the drone. We’re talking about high-resolution cameras, LiDAR scanners, thermal sensors, or agricultural sprayers. Often, these components are worth more than the drone itself.

For example, a construction firm flying a DJI Matrice 300 RTK might have $14,000 in hull value but be carrying a $6,000 thermal camera. A policy without specific payload coverage would leave that expensive sensor completely unprotected in a crash.

Key Takeaway: Hull and payload coverage are based on the stated value of your equipment. It's vital to insure your gear for its full replacement cost. The last thing you want after an accident is to find out you’re underinsured.

Advanced Coverage for Professional Operations

As your business grows, so does the complexity of your operations. You might find you need more specialised coverage to fill potential gaps in a standard policy.

Inland Marine Coverage

Don’t let the name fool you; this has nothing to do with water. Inland marine insurance protects your equipment while it's in transit on the ground or stored off-site. If your drone, controllers, and laptops get stolen from your locked work van, this is the coverage that kicks in. It’s all about protecting your assets when they aren't in the air.

Non-Owned or Leased Aircraft Coverage

Do you ever rent a specialised drone for a one-off job? Or maybe hire a freelance pilot who uses their own gear? Non-owned aircraft liability coverage extends your liability protection to drones that you use but don't personally own. This is an absolute must-have to ensure you're covered if an incident happens with a rented or subcontracted aircraft operating on your behalf.

Here’s a quick summary of when you’d need each type of coverage:

| If you... | Then you need... | To protect against... |

|---|---|---|

| Operate a drone for any client | Liability Coverage | Damaging client property or injuring a bystander. |

| Own your drone | Hull Coverage | The cost of repairing or replacing your aircraft after a crash. |

| Use expensive cameras or sensors | Payload Coverage | Damage to your valuable attached equipment during an incident. |

| Transport gear to job sites | Inland Marine | Theft of your drone and related equipment from your vehicle. |

| Rent drones or hire subcontractors | Non-Owned Coverage | Liability claims arising from an aircraft you don't personally own. |

By carefully selecting from these options, you can build a commercial UAV insurance policy that perfectly matches the risks you actually face. This way, you're fully protected without paying for extras you don't need, giving you the confidence to fly and grow your business.

Meeting Client and Regulatory Demands

While getting commercial UAV insurance is a smart move for any operator, let's be honest—it's rarely a choice. In the world of professional drone work, insurance is almost always a non-negotiable, driven by two major forces: your clients and the aviation authorities.

Most of the time, the push comes directly from the people paying your invoices. Any serious client in industries like construction, energy, or film production won't even entertain a conversation without seeing your Certificate of Insurance (COI). That piece of paper is your entry ticket to the big leagues, proving you can cover the costs if something goes sideways.

The Contractual Bottom Line

Crack open a contract from a corporate client, and you'll find an insurance clause tucked in there. This isn't just filler text; it’s a hard requirement spelling out the exact coverage you need to carry to even set foot on their property.

These clauses are all about protecting the client. They need to know that if your drone causes an accident on their site, they won't be left holding the bag. From their perspective, an uninsured drone operator is a massive financial gamble they're just not willing to take.

You’ll typically see a few standard demands:

- Minimum Liability Limits: Contracts will always name a minimum liability limit. $1 million is a very common starting point, but don't be surprised to see that number climb to $5 million or more for larger industrial jobs or government contracts.

- Additional Insured Status: Clients will insist on being added to your policy as an "additional insured." This gives them a direct line of protection under your coverage for any claims arising from your work.

- Waiver of Subrogation: This is a fancy way of saying your insurance company can't come after the client for money if they pay out a claim, even if the client was partially at fault.

A solid insurance policy does more than just satisfy a contractual obligation. It tells potential clients you're a serious, professional, and low-risk partner. Instantly, you're ahead of the competition.

Regulatory and Compliance Pressures

Beyond client contracts, you've got the aviation authorities to think about. Flying by the book is the bedrock of any safe, insurable drone operation. Just look at the general FAA commercial pilot license requirements; the level of detail shows just how seriously compliance is taken.

While rules like the FAA's Part 107 don't make insurance mandatory for every single flight, it’s often required for more complex operations. If you need a waiver to fly over people or operate at night, for example, regulators will almost certainly want to see proof of adequate liability coverage. It shows them you've thought through the financial risks.

If you want to go deeper on this, our commercial drone compliance guide is a great resource.

At the end of the day, having the right insurance is all about access. It gives you access to better clients, more complex projects, and the kind of operational approvals that are completely off-limits to uninsured pilots. Think of it less as a safety net and more as a key that unlocks the door to bigger opportunities.

How Insurers Calculate Your Premium

Ever wonder what goes on behind the curtain when an insurance company quotes you a price? It’s not a number pulled out of a thin air. Underwriters are professional risk assessors, and their whole job is to weigh a dozen different factors to figure out the odds of you filing a claim. The more risk they see, the higher your premium will be.

Think of it like getting a loan. A bank looks at your credit score, income, and debt to decide how risky you are. In the same way, an insurance underwriter examines your entire operational profile to calculate a "risk score" for your drone business.

Getting a handle on these factors is huge. It demystifies the pricing process and, more importantly, shows you exactly where you have the power to bring your costs down.

Your Drone and Its Mission

The very first thing an insurer will look at is your gear and what you do with it. This is especially true for hull and payload coverage, where the value of your hardware is a direct cost driver. A freelance photographer flying a $2,200 DJI Mavic 3 will naturally pay a lot less than a survey company operating a $20,000 DJI Matrice 300 RTK with a thermal payload. The math is simple: more expensive equipment costs more to replace if something goes wrong.

But it’s not just about the price tag. The nature of your work plays a massive role in their calculations.

- Low-Risk Ops: Think real estate photography or agricultural mapping in wide-open rural areas. Fewer people, less property, less risk.

- High-Risk Ops: Flying over crowded events, conducting inspections on active construction sites, or spraying chemicals all introduce a lot more variables. More variables mean more risk.

An insurer knows that a drone flying over a wedding has a much higher chance of causing a pricey liability claim than one mapping an empty field. It's all about context.

The commercial drone market is exploding, projected to jump from USD 12.81 billion in 2025 to USD 27.68 billion by 2032. This rapid growth is forcing insurers to get even more granular in how they assess operational risks. As missions get more complex, so do the premium calculations. You can dig into more insights on the expanding commercial drone market on MMRStatistics.com.

The Pilot Behind the Controls

Your experience and qualifications are just as important as the drone you fly. An underwriter wants to see proof that you’re a safe, competent, and professional operator. A pilot with a spotless flight record and thousands of logged hours is a much safer bet than someone who just got their Part 107 certificate last week.

Here’s what they’re looking for:

- Certifications: An FAA Part 107 certificate (or your country's equivalent) is the absolute minimum. Any advanced training credentials you have will strengthen your case.

- Flight Hours: More documented flight hours equals more proven experience. It’s that simple.

- Safety Record: A clean history, free of accidents or claims, is a massive plus. This is your number one ticket to more favourable rates.

This is where meticulous record-keeping stops being a chore and starts being a financial tool. Organised flight logs aren't just for compliance; they're solid proof of your professionalism and a key piece of data in your insurance application.

Your Coverage Limits and Location

Finally, the nuts and bolts of the policy itself will directly impact your premium. The higher you set your liability limits, the more the policy will cost. While a $1 million liability limit is pretty standard for many jobs, high-stakes industrial or government contracts might demand $5 million or more. That higher limit will, of course, increase your premium.

Where you fly matters, too. Operating mainly in dense urban environments is seen as far riskier than flying in quiet suburban or rural areas. There’s just more people and property to potentially damage. An operator working in downtown Chicago will almost certainly face a higher premium than one in rural Nebraska, even if every other factor is identical.

The key takeaway? All these factors—your gear, your mission, your experience, and your coverage needs—are interconnected. When you start to see how they fit together, you can stop viewing your insurance premium as a fixed cost. Instead, it becomes a dynamic figure you can actively manage through smart, safe, and well-documented operations.

Factors Influencing Your Insurance Premium

To make it even clearer, here’s a breakdown of the variables that insurers weigh up when they’re calculating your premium. Think of this as their underwriting checklist.

| Factor | Why It Matters to Insurers | Impact on Premium (Low/Medium/High) |

|---|---|---|

| Aircraft Value | Higher-value drones and payloads cost more to repair or replace, directly affecting hull and payload coverage costs. | High |

| Mission Type | Flying over people, near critical infrastructure, or in complex environments (e.g., construction sites) presents a greater liability risk. | High |

| Location of Operations | Dense urban areas have a higher concentration of people and property, increasing the potential for third-party damage claims. | High |

| Liability Limit | The higher the coverage amount you request (e.g., $5M vs. $1M), the greater the insurer's potential payout. | High |

| Pilot Experience | A long track record of safe, documented flight hours demonstrates proficiency and a lower likelihood of pilot error. | Medium |

| Claims History | A history of accidents or claims signals a higher risk profile to the underwriter. A clean record gets better rates. | Medium |

| Safety Procedures | Documented safety protocols, risk assessments, and maintenance logs show a commitment to risk mitigation. | Medium |

| Deductible Amount | A higher deductible means you take on more financial risk upfront, which can lower your premium. | Low |

Understanding this table gives you a roadmap. By actively improving in the areas you can control—like pilot experience, safety procedures, and meticulous record-keeping—you can present yourself as a lower-risk client and earn a better premium.

A Practical Checklist for Buying Your First Policy

Diving into the world of commercial UAV insurance for the first time can feel like a lot to handle. There are so many providers and endless policy options, so how do you know you're making the right call? The secret is to tackle it step-by-step, armed with the right info and the right questions.

This checklist breaks the whole process down into simple, manageable steps. If you follow this guide, you’ll be able to gather your essential documents, properly check out insurance providers, and compare quotes with real confidence. The goal is to land a policy that truly fits how you operate.

Step 1: Prepare Your Documentation

Before you even think about getting a quote, you need to get your house in order. Insurers will want a clear picture of your operations to figure out your risk level. Think of it like prepping your CV before a big job interview—the more organised and professional you look, the better impression you'll make.

Get the following documents and information ready to go:

- Pilot Certificates: Have copies of your FAA Part 107 certificate (or your country's equivalent) for every pilot you plan to cover.

- Drone and Payload Inventory: Make a detailed list of all your drones and the gear they carry. You'll need the make, model, serial number, and current replacement value for each and every item.

- Flight Logs: Be prepared to show a summary of your total flight hours and experience. Well-kept logs are solid proof of your professionalism and can definitely help lower your premium.

- Business Information: Have your official business name, address, and any registration numbers handy.

Step 2: Vet Providers and Ask the Right Questions

Let's be clear: not all insurance providers are created equal. You need to find a partner who genuinely understands the unique risks of the drone world, not just a general business insurer who tacks on a drone policy as an afterthought. Once you've got a shortlist of potential providers, it's time to dig in.

When you're on the phone with an agent, don't hold back. Ask specific, detailed questions. How they answer will tell you a lot about the quality of their coverage and whether it’s right for you.

Here are some critical questions to have in your back pocket:

- Does this policy cover data privacy and invasion of privacy claims? This is a huge one that often gets overlooked. It protects you if someone claims your drone’s camera snooped where it shouldn’t have.

- What are the specific exclusions I need to be aware of? Get them to point out the exact clauses that could get your coverage thrown out, like flying beyond visual line of sight (BVLOS) without a waiver or operating in restricted airspace.

- How do you handle claims for non-owned or rented drones? If you ever bring on freelance pilots or rent gear, you need to know precisely how your liability extends to those situations.

- Is your policy recognized for adding clients as an "additional insured"? This is a non-negotiable for most corporate gigs, and a slow or clunky process here can lose you work.

A provider's willingness to clearly explain their policy's fine print is a strong indicator of their expertise and transparency. If an agent is vague or dismissive of your questions, consider it a major red flag and move on.

By following this checklist, you turn buying insurance from a confusing chore into a smart business move. It ensures you don't just get covered, but you get the right coverage. That gives you the peace of mind to focus on what you do best—flying.

How Smart Operations Can Lower Your Insurance Costs

While the value of your drone and the kinds of missions you fly will always set a baseline for your commercial UAV insurance premium, your day-to-day habits have a massive impact. If there's one thing insurers love, it's predictability. A pilot who can prove they are safe, organised, and compliant is seen as a much lower risk than one who can't.

This is where operational excellence stops being a buzzword and starts putting money back in your pocket. By adopting smart, repeatable workflows, you can directly influence how an underwriter views your business, which can lead to better terms and lower costs.

Think about it. Would you rather walk into an insurer's office with a messy folder of loose papers, or with a clean, comprehensive digital record of your entire operation? This is the power of using a drone operations management platform like Dronedesk.

Turning Good Habits into Tangible Savings

An underwriter's job is to calculate risk based on the evidence you provide. When a pilot presents meticulous records, it paints a picture of a professional, risk-averse mindset. This isn't just about looking good—it's about giving them concrete proof that you're a safe bet.

Here’s how a systemised approach makes a real difference:

- Detailed Flight Logs: Consistent, detailed logs for every single flight demonstrate your experience and professionalism. They show you're a serious operator with verifiable hours, not just a hobbyist dabbling in commercial work.

- Maintenance Records: A complete history of maintenance checks, firmware updates, battery cycles, and repairs proves you’re proactive about equipment safety. This drastically reduces the perceived chance of an accident due to mechanical failure.

- Pilot Credentials: Keeping pilot licences, training certificates, and medical info in one easily accessible place shows your team is qualified and current on all regulations.

- Pre-Flight Risk Assessments: Documenting your risk assessments for every mission is the single best way to show a deep-rooted commitment to safety. It's your proof that you think before you fly.

By presenting this level of organised data, you shift the conversation with your insurer from a subjective chat to an evidence-based case. You're no longer just telling them you're reliable; you're proving it. That's exactly what they want to see.

This disciplined, data-backed approach to risk management is precisely what underwriters are trained to look for when pricing a policy.

Speeding Up Claims with Organised Data

The payoff for keeping meticulous records doesn't stop once you've secured your policy. Should the worst happen and you need to make a claim, the quality of your documentation can be the difference between a quick payout and a drawn-out nightmare.

When an incident occurs, your insurer will immediately launch an investigation. They’ll request everything: flight logs, maintenance history, the weather conditions at the time, and the pre-flight risk assessment you completed for that specific mission. If your records are incomplete or scattered across different notebooks and spreadsheets, the claims process can drag on for weeks or even be denied.

On the flip side, having all this data neatly organised in a platform like Dronedesk means you can generate a complete incident report almost instantly. This immediately demonstrates due diligence, proves you followed proper procedures, and helps ensure a fair and swift settlement. You can learn more about how all these factors connect in our complete guide on what drone insurance costs.

This level of organisation not only strengthens your claim but also reinforces your status as a responsible, low-risk operator, which will pay dividends when it's time for your renewal.

A Few Final Questions About Drone Insurance

Even after you've got a handle on the basics, a few specific questions tend to pop up just as you're ready to pull the trigger on a policy. Let's tackle those last few uncertainties so you can move forward with total confidence.

Can I Get By With On-Demand Insurance Instead of an Annual Policy?

Pay-per-flight, or on-demand, insurance can be a fantastic way to dip your toes in the water. If you're just starting out and only have occasional, sporadic jobs, it offers incredible flexibility without a big upfront cost. Think of it as the perfect entry point for testing the commercial drone market.

But here's the thing: as your business grows and your flight schedule fills up, an annual policy almost always makes more financial sense. More critically, if you're working with corporate clients, they'll often demand to be listed as an "additional insured" for the entire project timeline. That kind of continuous coverage is something only an annual policy can provide.

Does My Policy Cover Me If I Fly in Other Countries?

This is one detail you absolutely cannot afford to get wrong. The vast majority of standard commercial UAV policies are territory-specific. That means your UK policy covers you in the UK, and your US policy covers you in the US—and that’s it.

If an exciting international project comes your way, you have to talk to your provider. You’ll need to see if they can offer a global coverage extension or if you're required to buy a separate, local policy for the country you'll be operating in. Never, ever assume your domestic policy has your back when you're abroad. Aviation laws and insurance rules change dramatically from one country to the next.

A classic rookie error is assuming your insurance is universal. Before you even think about accepting international work, verify your policy's geographic limits. Not doing so could leave you exposed to a staggering, uninsured liability risk.

What Actually Happens If I Need to Make a Claim?

If an incident does occur, the first thing you do is make sure everyone is safe. Once that's handled, your next job is to become a world-class documentarian. Start taking photos and videos of the scene from every angle, get contact details from anyone who saw what happened, and secure your drone if it's safe to do so.

Then, contact your insurance provider as soon as you possibly can to report the incident. This is the moment where all your hard work maintaining organised records pays off big time. The insurer will want to see your flight logs, pre-flight risk assessments, maintenance history, and a detailed written statement of the event. Having this information organised and ready to go will massively speed up the claims process and immediately show the adjuster you're a true professional.

Ready to manage your drone operations with the kind of professionalism that insurers love to see? Dronedesk gives you the tools to meticulously log flights, track maintenance, and document risk assessments, all in one place. Simplify your compliance, streamline your underwriting process, and fly with confidence by visiting https://dronedesk.io to start your free trial today.

How to Pass the FAA Drone Written Test First Time →

How to Pass the FAA Drone Written Test First Time → What a BVLOS Flight Means for Risk and Compliance →

What a BVLOS Flight Means for Risk and Compliance → Drone VLOS Rules Explained for Commercial Teams →

Drone VLOS Rules Explained for Commercial Teams → FAA Remote ID Rule Explained for Commercial Pilots →

FAA Remote ID Rule Explained for Commercial Pilots → Drone Legal Requirements for Commercial Operations →

Drone Legal Requirements for Commercial Operations → Drone Near Airport Rules Explained for Safer Planning →

Drone Near Airport Rules Explained for Safer Planning → International Drone Regulations Every Global Team Should Know →

International Drone Regulations Every Global Team Should Know → Drone Flight Risk Assessment Example for Safer Missions →

Drone Flight Risk Assessment Example for Safer Missions → Beyond Visual Line of Sight Explained for Operators →

Beyond Visual Line of Sight Explained for Operators → How BVLOS Drone Operations Change Commercial Workflows →

How BVLOS Drone Operations Change Commercial Workflows →